A Mayan Financial Crash

The Case of Nebaj

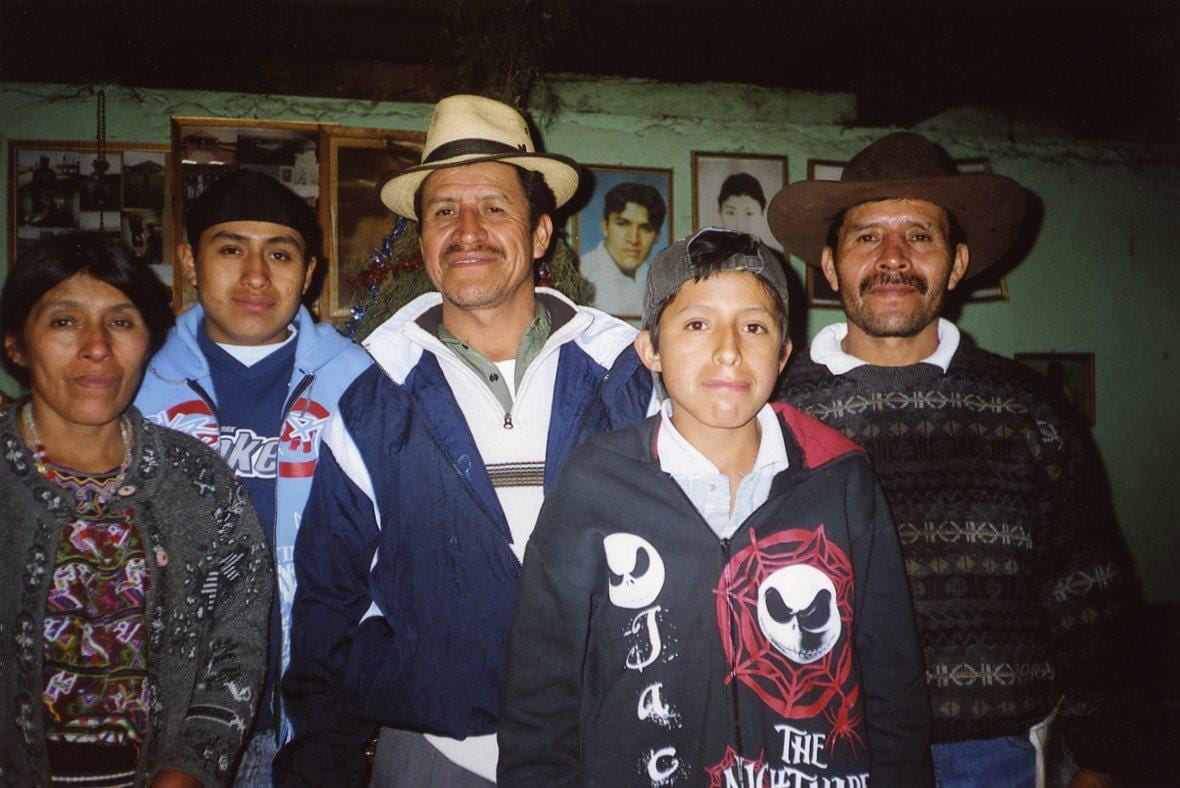

Nebaj community members: people become commodities. Photo by David Stoll

Next to an ancestor cross, where Ixil priests make regular offerings, lives one of Nebaj’s better-known financial speculators. Doña Alfonsa (not her real name) has eight children and sells food in the market. She doesn’t own a motor vehicle but she does have a cell phone. Her story is well-known because she has repeatedly apologized for it. In 2005, Alfonsa and her husband began asking their neighbors for huge loans. They offered to pay interest of 10% and 15% per month and presented their house and agricultural land as collateral. Then they transferred the funds to four acquaintances who promised them interest of 15% and 20% per month. Of their four business partners, three were K’iche’ Mayas who said they were guiadores de préstamos (roughly, loan advisers) sending local men to work in the United States. The fourth, an Ixil village leader and former functionary of the Guerrilla Army of the Poor, said that he needed seed money to attract an international aid project. And so the couple borrowed circa Q500,000 (at 7.8 quetzals to the dollar, US$64,000) and turned it over to the four. They expected to reap millions.

What they didn’t know is that their partners invested the funds in, not emigrants or projects, but a Mam Maya priest who promised riches from the volcanoes of Quezaltenango. At last report, this spellbinding practitioner of Mayan tradition was the object of an arrest warrant, a problem that was not interfering with his used-car business on the Mexican border. Back in Nebaj, the title to Alfonsa’s house fell into the hands of a bank, she was summoned to court, and she was about to lose her house when the bank agreed to refinance Q225,000 of the debt. She and her family will be able to keep their home as long as they make mortgage payments of Q3,000 a month. The only way they can generate Q36,000 (US$4,600) a year is in the U.S. labor market, to which end Alfonsa’s husband has joined their son in Houston, where the two are washing dishes in restaurants but having trouble finding enough hours. If they hang on in the United States, and if they remit faithfully, their house will be in the clear as early as 2024.

If you had told me this story a few years ago, I wouldn’t believe you. How can Guatemalans with household incomes of $1500 or so per year make $10,000 loans? How can they charge each other monthly interest rates of 10%, 15%, even 20%? How can they believe that wealth comes from volcanoes? Last but not least, how can their scramble to earn dollars in the U.S. make them poorer? These are not easy questions, but the answers lead back to two sacred cows in the current pantheon of wishful thinking: 1) microcredit and 2) unauthorized border-crossing in search of a better life.

Nebaj was hit hard in Guatemala’s civil war (it’s one of the towns for which genocide lawsuits have been filed), and it has received more aid projects than any other Mayan town. Yet no amount of aid will address a basic problem. Thanks to vaccination campaigns and potable water projects, most children are surviving to adulthood. Nebaj parents have been slow to reduce their pregnancies, women still average six children and the population is approaching five times what it was before the Spanish Conquest. The land base has become so fractured that most Nebajenses do not inherit enough land for subsistence farming. Local jobs pay four to eight dollars a day, which is enough to feed a family but not enough to pay for the consumer goods that Nebajenses now admire and want.

So in the 1990s the aid agencies introduced the gospel of microcredit—why not just loan the Nebajenses money? This would avoid the many accountability problems of communal projects and enable each household to devise its own solutions. Loaning money seemed like such a good idea that, by 2008, Nebajenses could borrow from at least twenty-three different projects, microcredit agencies, savings–and-loans, and banks. One problem to which the lenders didn’t give enough attention was, exactly what were Nebajenses going to do with all that credit? Presumably they were going to become bold entrepreneurs, which is why Nebaj now features hundreds of retail outlets without enough customers.

Opening modest lines of credit to Nebajenses was a good idea. But pumping large amounts of credit into a crowded mountain environment with few agricultural or industrial possibilities was, in retrospect, not such a good idea. No one has been able to come up with a game plan for turning Nebaj into a high-productivity consumer economy. The most exportable commodity that Nebaj produces is labor. And so Nebajenses had a better idea—why not invest my loans in exporting the single product that I possess in abundance to a distant market where this product will be in demand? And so Nebajenses exported themselves to the United States. Me urge ir a los Estados Unidos, men told their wives. And so the Nebajenses joined an estimated 1.5 million Guatemalans who are now in the United States, the majority without legal authorization.

Some of Nebaj’s first wage pilgrims to go north were very successful. Most of the migrants are males between the ages of fifteen and thirty, along with some older men and a small minority of women. From fragmentary remittance data, I estimate that something like 4,000 Nebajenses were in the United States in late 2007 and early 2008. That would be 5.7% of the Nebaj population and 20-25% of the male workforce over the age of 15. In the peak year of 2007 I further estimate that Nebajenses sent back $22 million, which would be $300 for every man, woman and child in the municipio. Since $300 is roughly the annual per capita income, the remittances were a tremendous multiplier of the money in circulation. And yet this tidal wave of prosperity was a shock wave for every household that did not have a wage earner in the United States. The price of houses, building lots and agricultural land shot sky high. Nebaj experienced a bubble economy because the inflow of donations, credits and remittances led to enormous price hikes for assets that are in fixed supply. Hyperinflation meant that anyone who wanted to buy land would have to undertake all the risks of seeking work in the United States.

With inflation like this, every household in Nebaj is under pressure to send someone north. Not every household has done so, and not every household will, but every household has thought about it. Thus the prosperity of some Nebajenses has meant deep anxiety for others. Remaining faithful to the routines of peasant subsistence means being left behind. For those who are too poor or too old to head north, the most obvious beacon of hope is a pyramid scheme. This is what snared Doña Alfonsa and her husband. In Guatemala get-rich-quick schemes combine the language of non-governmental organizations and development projects with the ritual supplications of folk Catholicism. But the crux of many a scheme is human smuggling into the U.S. labor market. All told, the Nebajenses have sunk millions of dollars from loans, land sales and remittances into the $5,000 per head smuggling fees which Guatemalan-Mexican smuggling networks charge to bring them to safe houses in Phoenix, Arizona.

It is not just migrants who are lunging for the fabled riches of wage labor in El Norte. A less demanding way to partake of El Dorado is to stay at home and become a moneylender. I know five market women who have borrowed money from multiple credit institutions, typically at 2% interest per month, in order to lend it to migrants at 10% per month. They live off the difference until the migrants fail to repay. The chains of debt between migrants, moneylenders and other peasant investors extend deep into families because the collateral securing a loan belongs to a spouse, parent, or sibling. The “immigrant bargain” is how scholars refer to these transactions–a quid pro quo in which a family takes on debt to establish members in a more remunerative labor market. The financial stakes are so high that intimate kin relationships are monetized and the family takes on the attributes of an export business.

Once a kin network is in debt, the only way it can keep up with payments is by maintaining wage earners in the United States. If we widen the concept of debt to deficits real or perceived, including the relative deprivation that human beings feel when their peers outstrip them in consumption and status, remittances from the United States are an engine for multiplying needs that can be met only by sending members of each household north. Nothing on the local economic horizon can pay for these aspirations. Yet in the United States, Nebaj’s wage pilgrims have been failing to find enough work since 2006. Even before our current economic recession, they were saturating the ethnic niches for their labor. When they can’t find enough work to pay back their debts, migration has the paradoxical effect of swallowing their assets back home.

Since 2008 remittances have plunged. Judging from remarks at various agencies, remittances are roughly half what they were at the peak. Default rates have climbed into double digits and dozens of foreclosures clog the docket at the local courthouse. Nebajenses are still going north, but in smaller numbers. The price of real estate has collapsed, making it impossible for creditors to recover their capital. And so the bubble has turned into Nebaj’s own version of the global credit crisis. In an uncanny anticipation of the U.S. derivatives’ bubble and how it burst, Ixil speculators borrowed other people’s money to multiply their gains, but only by incurring risks that are now bankrupting them and their creditors.

Microcredit, we have been assured, enables the poor to make headway against poverty. But debt has long functioned as a way to encourage poor people to “capitalize” their activities and, when they fail, separate them from their property. We also would do well to question whether there is enough employment in the United States for all the people who want to come here. Whether or not it is a good idea for Guatemalans to come north depends on whether the U.S. economy can provide them with stable jobs. Without stable jobs, they will be unable to recoup the cost of getting here and living here, endangering whatever property they have used as collateral. We should stop assuming that coming to the United States is a benefit for Guatemalans and their families.

Fall 2010 | Winter 2011, Volume X, Number 1

Related Articles

Guatemala: Editor’s Letter

The diminutive indigenous woman in her bright embroidered blouse waited proudly for her grandson to receive his engineering degree. His mother, also dressed in a traditional flowery blouse—a huipil, took photos with a top-of-the-line digital camera.

Making of the Modern: An Architectural Photoessay by Peter Giesemann

Making of the Modern An Architectural Photoessay by Peter Giesemann Fall 2010 | Winter 2011, Volume X, Number 1Related Articles

Increasing the Visibility of Guatemalan Immigrants

Guatemalans have been migrating to the United States in large numbers since the late 1970s, but were not highly visible to the U.S. public as Guatemalans. That changed on May 12, 2008, when agents of Immigration and Customs Enforcement (ICE) launched the largest single-site workplace raid against undocumented immigrant workers up to that time. As helicopters circled overhead, ICE agents rounded up and arrested …

{kind=link}